Process interview demo Video

Building permits: submission to certificate of occupancy

A plans examiner maps multi-department review, resubmit loops, inspections, and final sign-off.

WatchAn order management and credit/AR lead at a mid-size wholesale distributor walks order-to-cash end to end: from multi-channel order capture through credit holds, fulfillment, and invoicing into the deductions, collections, and cash application where DSO and write-offs really live.

Interviewer: Thanks for doing this. I want to walk through your order-to-cash process end to end, the way you'd explain it to someone new. Wherever you want to start.

Order & AR lead: Sure. So order-to-cash, for us, is everything from the moment an order shows up to the moment the cash is actually applied against the invoice. People think of it as "take the order, ship it, get paid," and it mostly is, but there's a lot of detail in the middle and honestly the back half is where it gets interesting. Let me start at the front, which is order capture.

Interviewer: How do orders come in?

Order & AR lead: Every way you can imagine. Our bigger customers send EDI, which drops straight into the ERP, clean. Some use our web portal. But we still get a ton by email, and a fair number by phone: a rep calls it in, or the customer does. Anything that's not EDI or portal, one of our CSRs is keying it into the ERP by hand. So right away you've got two worlds: the automated channel and the manual channel, and the manual channel is where typos and missed lines happen.

Interviewer: Okay, the order's in the system. Then what?

Order & AR lead: Then we validate it. Are the item numbers real, are the units of measure right. That one bites people, you order a case versus an each and it's a tenfold difference. And pricing, which for us is a big one, because most customers have contract pricing, special deals, volume tiers. So we're checking the order price against what their contract says. If there's a mismatch, or it doesn't tie to their PO, we put it on hold and go back to them before it moves.

Interviewer: And then it ships?

Order & AR lead: Not yet. Next is credit. Every order gets screened against the customer's credit limit and their AR aging. If they're over their limit, or they've got invoices well past due, the order goes on credit hold. And then it's the credit team's call: release it, cut it down, or ask for prepayment. This is honestly one of the friction points internally, because sales wants the order to ship, credit wants to get paid, and the customer's in the middle. That tension is just part of the job.

Interviewer: Makes sense. So credit clears it.

Order & AR lead: Credit clears it, and now we check availability. Can we actually fill it from stock. We allocate the inventory. If we're short or out, there's a branch: we backorder it, offer a substitute, pull it from another distribution center, or in some cases drop-ship it straight from the vendor. Then we send the customer an acknowledgment: here's what's confirmed, here's the price, here's when it's coming. EDI customers get an 855, everyone else gets an email.

Interviewer: Then it goes to the warehouse.

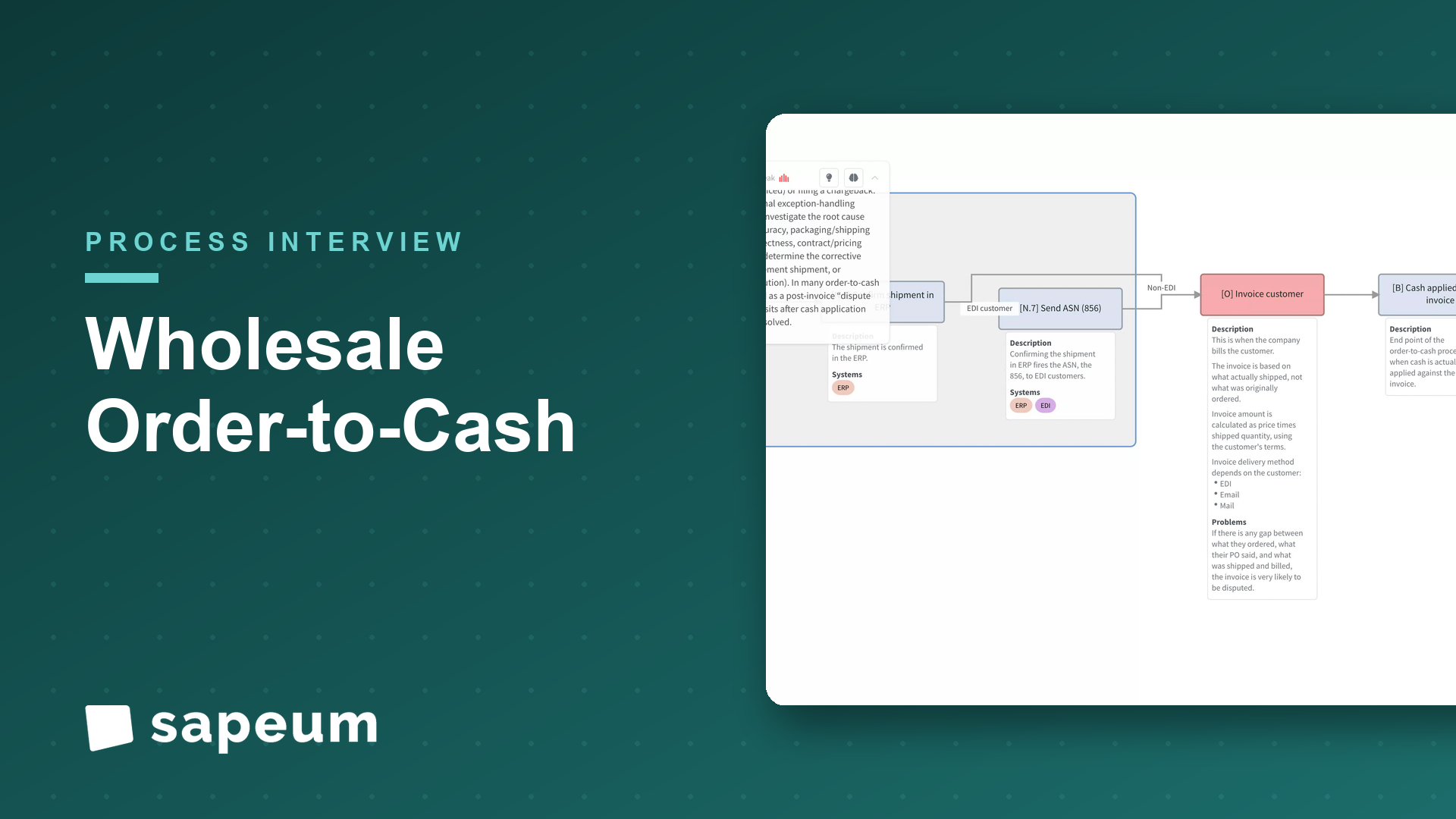

Order & AR lead: Right, the pick ticket releases to the warehouse, they pick it, pack it, stage it. If there's a short pick: they go to grab it and the count's off. We decide whether to ship partial or hold for complete, which depends on the customer. Then shipping. We pick the carrier, generate the BOL and labels, it goes out, we capture tracking. Parcel, LTL, sometimes the customer sends their own truck. Freight terms decide who's paying for it. And we confirm the shipment in the ERP, which fires the ASN: the 856; to the EDI customers.

Interviewer: And that's when you bill them.

Order & AR lead: That's when we invoice, yeah. And the key thing is we bill off what actually shipped, not what was ordered: price times shipped quantity, with their terms. Goes out by EDI, email, or mail depending on the customer. And here's where I'd flag the first real leak: if there's any gap between what they ordered, what their PO said, and what we shipped and billed, that invoice is going to get disputed. Almost guaranteed.

Interviewer: Tell me about the disputes.

Order & AR lead: So the customer receives the goods, and they match our invoice against their PO and their receiving. If something's off: they got short-shipped, something came damaged, the price doesn't match what they expected. They take a deduction or file a chargeback. Meaning they just pay us less, and now we've got to figure out why. We research it, and if they're right we issue a credit memo, maybe an RMA if product's coming back. The big-box and national accounts are very good at deductions, let me put it that way. That's a whole work stream by itself.

Interviewer: And meanwhile you're tracking what's owed.

Order & AR lead: Right, AR aging. We're watching every open invoice, sending statements and reminders as things come due. Anything that goes past due rolls toward collections. Collectors work those accounts: calls, emails, sometimes a payment plan, and if it gets bad enough we put them back on credit hold or hand it to an agency. Nobody loves that part but it's necessary.

Interviewer: And then the money comes in.

Order & AR lead: Money comes in: check, ACH, wire, credit card, lockbox, all of it. And then the step people underestimate the most: cash application. We have to take that payment and apply it against the right invoices. When a customer pays one invoice in full with clean remittance, easy. But a lot of them pay fifty invoices in one lump with a deduction on six of them and remittance detail that doesn't quite line up. So somebody's sitting there matching payments to invoices, chasing down what a short-pay was for, parking what we can't match as unapplied cash. That matching is genuinely where a lot of the manual time goes.

Interviewer: And then you close it out.

Order & AR lead: Then we close the order, reconcile the AR, and report on it: DSO, our deduction rate, write-offs. And that reporting loops back: if a certain customer is always taking deductions, or a certain item keeps getting disputed, that should feed back into how we price it, how we set their credit, how we set them up. When that loop actually works, the next quarter's cleaner.

Interviewer: So if you had to name the thing people get wrong about order-to-cash: what is it?

Order & AR lead: They think the order is the hard part. Get the order in, get it out the door, you're done. But the order's the easy half. The money leaks in the back half: the deductions, the short-pays, the cash that sits unapplied because nobody can match it. Your DSO and your write-offs live there, not in order entry. And a lot of that back half is still people in spreadsheets reconciling things by hand, matching remittance line by line. So if you want to actually move the number, that's where the opportunity is: tightening up the credit-to-cash side, not the taking-orders side. That's the part I'd want help with.

Interviewer: That's a great place to end it. Really helpful, thank you.

Order & AR lead: Anytime. It's a process with a lot of moving parts, so, happy to walk through it.

Keep exploring

A plans examiner maps multi-department review, resubmit loops, inspections, and final sign-off.

Watch

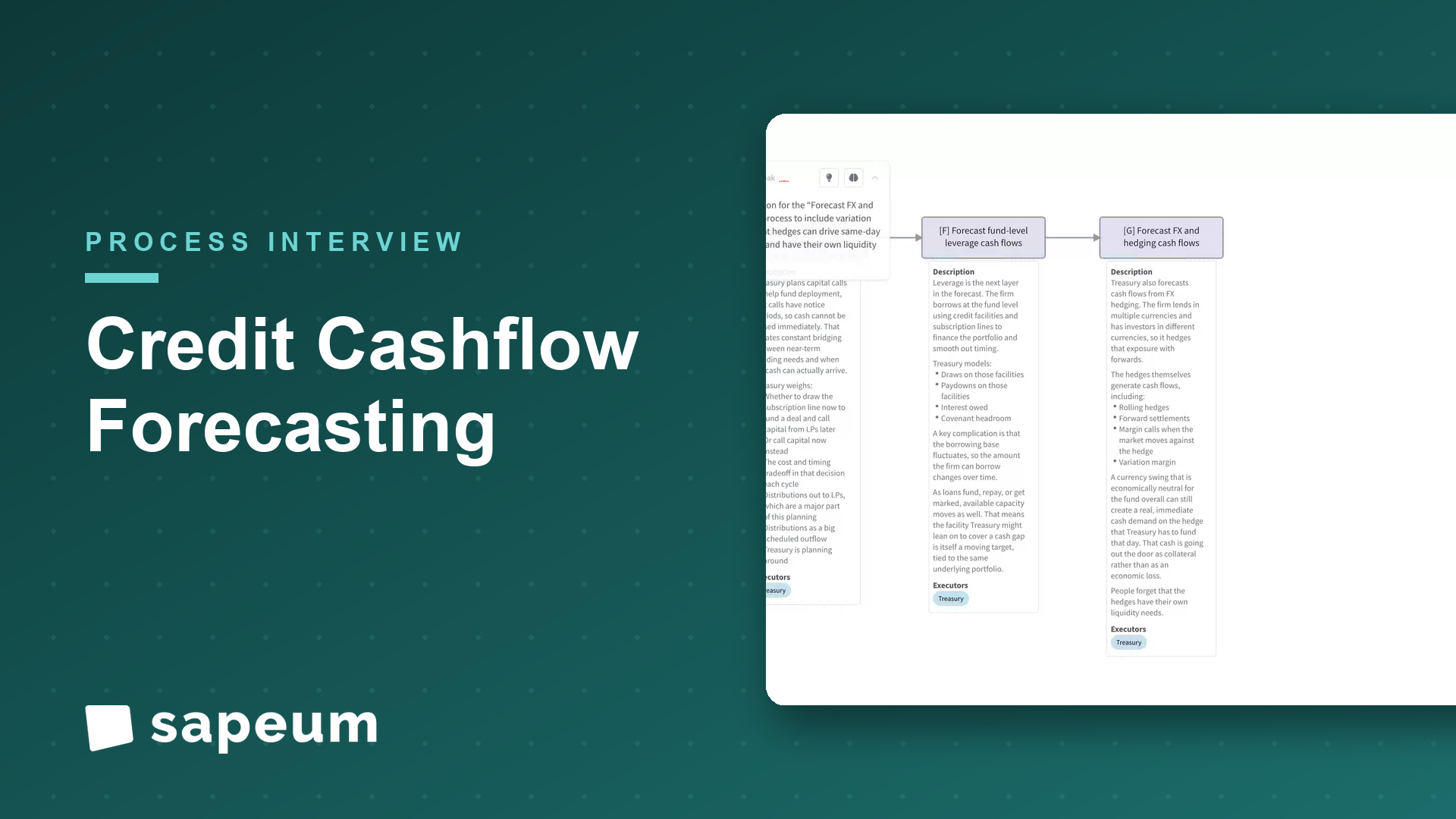

A treasury lead maps cash forecasting across funds and entities, and where it breaks down.

Watch

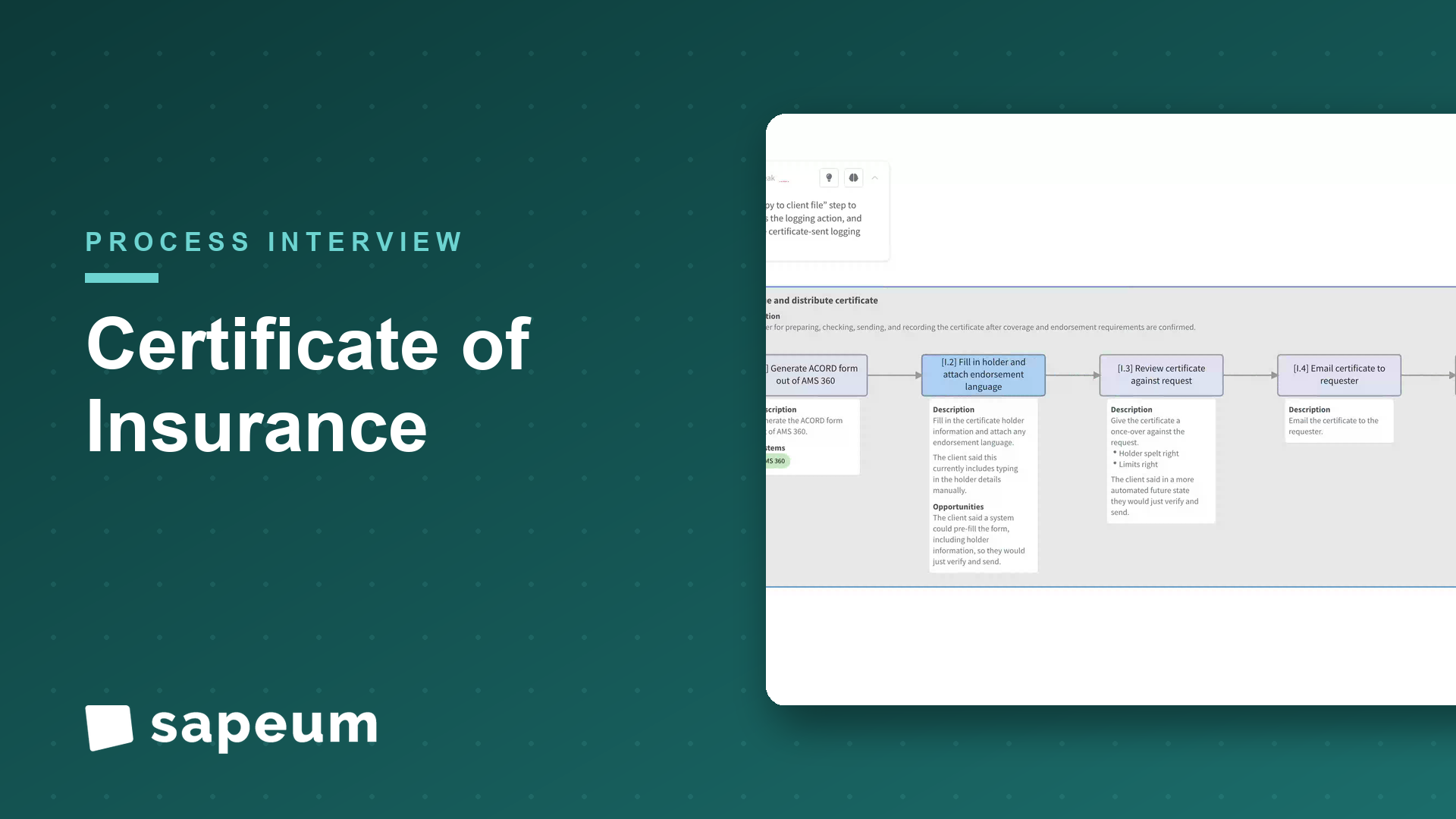

A brokerage account manager walks through COI issuance while the process maps itself; including the automation nobody had scoped.

WatchSapeum is designed with enterprise-grade security practices from the ground up: encryption at rest and in transit, role-based access controls, and auditable change history.

Everything you just saw runs on real workshops, not staged demos. Bring a process of yours and see for yourself.

Request a demo