Process interview demo Video

Building permits: submission to certificate of occupancy

A plans examiner maps multi-department review, resubmit loops, inspections, and final sign-off.

WatchA treasury / fund-finance lead at a private-credit manager walks through forecasting cash across funds and entities: horizon, current position, forecasting fundings (delayed draws, revolvers), repayments and prepayments, the leverage facility and borrowing base, capital calls and distributions, FX hedging and margin calls, aggregation, gaps, funding actions, stress testing, execution, and reconciliation.

Interviewer: Thanks for doing this. I'd love to walk through how you forecast cash, end to end, the way you'd explain it to a new person in treasury. Wherever you want to start.

Treasury: Sure. I'll set this up honestly, because it frames everything. Cashflow forecasting in private credit is hard. Harder than people expect. In a lot of businesses, forecasting cash is mostly a calendar exercise, you know what's coming in and what's going out. In credit, a huge share of the flows are at someone else's discretion, or they move with the market. Borrowers decide when to draw and when to prepay, our own leverage moves with the portfolio, and our currency hedges throw off cash when rates move. So I'm forecasting a system full of optionality I don't control. Let me start with the setup.

Interviewer: The setup being the forecast itself?

Treasury: Right. We run a rolling forecast, pretty granular in the near term, call it a thirteen-week view with daily detail for the next stretch, then quarterly further out. And it's by entity and by currency, which matters a lot here, because we're not one pool of cash, we're many. Then we anchor on the current position. Actual bank balances by account and currency, what capacity we have left on our facilities, and how much LP capital is still uncalled. Always start from actuals.

Interviewer: And then you project forward. What's first?

Treasury: Deployment, the cash going out to fund loans. And this is the first hard one. It's not just new deals in the pipeline. We have existing commitments where the borrower controls the timing. Delayed-draw term loans, revolvers. The borrower can pull that money when they want, within the terms. So I've got committed-but-undrawn capital that could get drawn next week or next quarter or never, and I have to forecast it probabilistically. There's no date in a calendar for it.

Interviewer: So you're estimating when borrowers will draw.

Treasury: Estimating, yeah, based on history and what we know. Same problem in reverse on repayments. We've got scheduled amortization and interest, which is the easy part, but then prepayments. Borrowers refinance and pay us back early, often when rates move or they get bought. A big unexpected prepay is a flood of cash in, which sounds great until you realize you now have to redeploy it or you're earning nothing on it. And some of our interest is PIK, paid in kind, it accrues rather than paying cash, so income on paper isn't always cash in the door.

Interviewer: You mentioned leverage too.

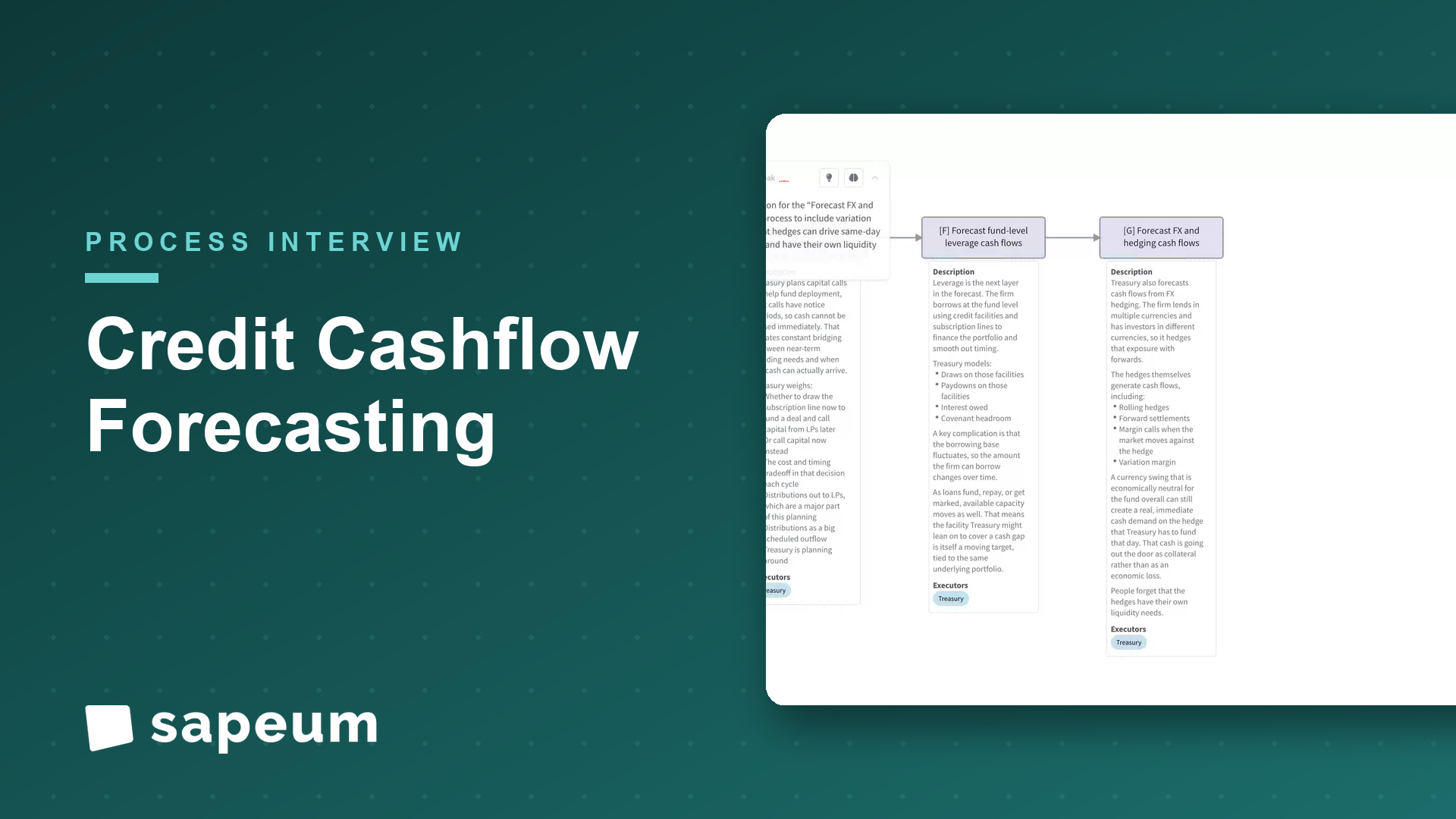

Treasury: Leverage is the next layer. We borrow at the fund level, credit facilities, subscription lines, to finance the portfolio and smooth out timing. So I'm modeling draws and paydowns on those facilities, the interest we owe, and our covenant headroom. And here's the tricky bit. The amount we can borrow, the borrowing base, fluctuates with the portfolio itself. As loans fund, repay, or get marked, our available capacity moves. So the thing I'd lean on to cover a cash gap is itself a moving target, tied to the same portfolio.

Interviewer: And capital calls fit in here?

Treasury: Right, capital calls and distributions. I plan calls to fund the deployment, but calls have notice periods, you can't just snap your fingers and have cash tomorrow. So there's constant bridging. Do I draw the subscription line now to fund a deal and call capital from LPs later, or call now? That's a cost and timing decision every cycle. And distributions out to LPs are a big scheduled outflow I'm planning around.

Interviewer: And then the currency piece.

Treasury: The FX and hedging, yes, and this one surprises people the most. We lend in multiple currencies and we have investors in different currencies, so we hedge that exposure with forwards. But the hedges themselves generate cash flows. They have to be rolled, forwards settle, and the one that bites, if the market moves against the hedge, we get a margin call. Variation margin. So a currency swing that's economically neutral for the fund overall can still produce a real, immediate cash demand on the hedge that I have to fund that day. That's cash going out the door for something that isn't a loss, it's just collateral. People forget the hedges have their own liquidity needs.

Interviewer: So now you pull it all together.

Treasury: Then I aggregate. All the inflows and outflows, by currency, by entity, by date. And I look for the gaps and the surpluses. Where am I short, in which currency, on which day, and where do I have idle cash piling up. A shortfall I have to fund. A surplus I want to sweep or put to work. Then I decide the funding actions. Draw the sub-line, call capital, sweep cash, roll or adjust a hedge, move money between entities or currencies, whatever's the cheapest reliable source for that need.

Interviewer: Is there a stress component?

Treasury: Always, given everything I just described. I stress it. What if a big prepay lands, what if a hedge margin call spikes, what if three revolvers get drawn in the same week, what if a capital call slips a few days. Any one of those is survivable. A couple at once is how you get caught short. So the stress testing is really about sizing the liquidity buffer. How much dry powder and facility headroom do I keep so I'm never forced into an expensive scramble. Then treasury and the CFO review and approve the plan, we execute, capital call notices, facility draws, hedge trades, wires, all respecting notice periods, and then we reconcile actuals against the forecast and tune the assumptions. Draw rates, prepay speeds, hedge sensitivity. And we do it again, because it rolls.

Interviewer: So if you had to name the thing people get wrong about cash forecasting, what is it?

Treasury: They think it's a spreadsheet of known ins and outs, that with enough diligence you can just predict it. In credit you can't, because the biggest flows aren't yours to control. The borrower decides when to draw and when to prepay. The market decides when your hedge needs margin. Your borrowing base moves with the very portfolio you're trying to finance. So the job isn't precise prediction. It's managing optionality. It's probabilistic forecasting, sizing the right liquidity buffer, and always knowing your cheapest next source of cash. And honestly the hardest practical part is that all of this, the entities, the currencies, the facilities, the hedges, lives across a stack of linked spreadsheets that are fragile and manual. So when something moves, re-running the whole picture quickly is genuinely painful, and that's exactly where I think there's a better way.

Interviewer: That's a great place to end it. Really helpful, thank you.

Treasury: Of course, happy to. It's a part of the business that's a lot more dynamic than it looks from outside, so it's good to lay it out.

Keep exploring

A plans examiner maps multi-department review, resubmit loops, inspections, and final sign-off.

Watch

A brokerage account manager walks through COI issuance while the process maps itself; including the automation nobody had scoped.

Watch

A CRA walks through how a trial really runs: startup, enrollment, monitoring, lock. And where it goes wrong.

WatchSapeum is designed with enterprise-grade security practices from the ground up: encryption at rest and in transit, role-based access controls, and auditable change history.

Everything you just saw runs on real workshops, not staged demos. Bring a process of yours and see for yourself.

Request a demo