Process interview demo Video

Building permits: submission to certificate of occupancy

A plans examiner maps multi-department review, resubmit loops, inspections, and final sign-off.

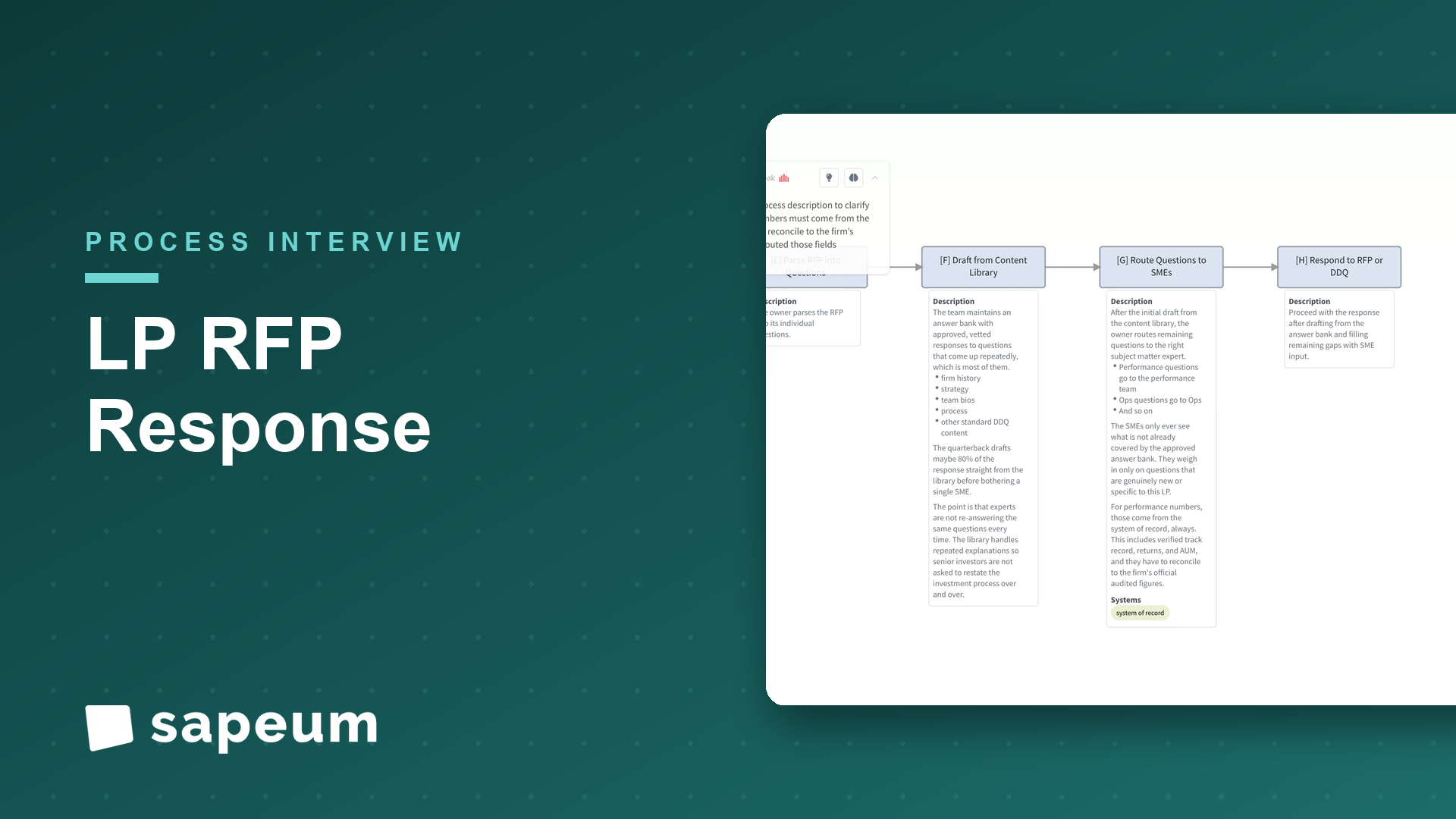

WatchAn RFP / proposals lead in IR walks through how the firm answers LP RFPs and DDQs: receive, go/no-go triage, quarterback, parse and route, draft from the content library, pull SME input on gaps only, add performance data, compliance review, assemble, submit, follow up, and update the library; balancing a firm-wide response against the investment team's time.

Interviewer: Thanks for doing this. I'd love to walk through how the firm responds to an LP RFP, start to finish, the way you'd explain it to a new person on the proposals team. Wherever you want to start.

RFPLead: Sure. So the thing to understand about RFPs and DDQs, due diligence questionnaires, is that a single one can touch the entire firm. Investment, performance, operations, compliance, legal, ESG, IR. Hundreds of questions sometimes. And they all have deadlines. So the central challenge of my job isn't the writing. It's mobilizing the firm to respond without burning the firm down in the process. Because if every questionnaire pulls our senior investment people off their actual jobs for a week, we'd never invest anything. Let me start when one arrives.

Interviewer: They just come in?

RFPLead: They come in. From a prospect, an existing LP doing fresh diligence, or a consultant who's gatekeeping for their clients. We log it. And then the most important step, the one people want to skip: go or no-go. Do we even respond to this?

Interviewer: You don't respond to all of them?

RFPLead: We can't, and we shouldn't. That's the discipline. Is this a real opportunity, is it a fit for what we do, do we have realistic odds, is it strategic? If it's a long shot or a bad fit, we decline politely, or we send a light-touch response, but we do not mobilize the whole firm for a deal we're not going to win. Saying no to the wrong RFPs is how you protect your ability to do a great job on the right ones. That gate is everything.

Interviewer: Okay, say it's a go.

RFPLead: Then we log the specifics. The deadline, the format, the submission portal, page limits, any mandatory sections. And we assign a quarterback. One person owns this response end to end. Not a committee, one owner. Then that person parses the RFP into its questions and routes each one to the right subject-matter expert. Performance questions to the performance team, ops questions to ops, and so on.

Interviewer: And then everyone writes their part?

RFPLead: No, and this is the part that makes it survivable. We draft first from the content library. We maintain an answer bank, approved, vetted responses to the questions that come up over and over, which is most of them. Firm history, strategy, team bios, process, all the standard DDQ content. So the quarterback drafts maybe eighty percent of the response straight from the library before bothering a single SME. The SMEs only ever see what's genuinely new or specific to this LP.

Interviewer: So the experts aren't re-answering the same questions every time.

RFPLead: Exactly, and that's the whole game. A senior investor's time is the scarcest thing in the building. If I make them re-explain our investment process for the fortieth time this year, that's malpractice on my part. The library does that. They only weigh in on a genuinely new question, and sometimes that does need fresh data or a real approval, which is fine, because now they're spending their time on the ten percent that actually needs them.

Interviewer: What about the performance numbers?

RFPLead: Those come from the system of record, always. Verified track record, returns, AUM, and they have to reconcile to our official, audited, GIPS-compliant figures. We never let someone eyeball a number into an RFP. Consistency matters enormously here, because consultants compare your answers across time and across documents, and if your numbers drift, you've got a credibility problem. Then compliance and legal review the whole thing. Accuracy, any regulatory claims, the right disclaimers, confidentiality. If something's flagged, we revise.

Interviewer: And then it gets assembled.

RFPLead: Then we assemble it into one document, edit it so it reads in one voice instead of like twelve people wrote it, and tailor it to this specific LP. Senior sign-off, the IR lead, sometimes someone from the deal side or an exec. Then we format it to their requirements, fill in their portal or their template, and submit before the deadline. The portals can be their own little adventure, odd formats, attestations, character limits, so we leave time for that.

Interviewer: Is that the end?

RFPLead: Usually there's follow-up. Clarifying questions, sometimes a finals presentation in person. Then the outcome, win or lose, and we log it along with any feedback we can get. And then the step that's easy to skip when you're exhausted and already onto the next one: we update the library. Any new approved answer we wrote goes back into the answer bank, and we refresh the content that goes stale, performance, AUM, bios, on a cadence. So the next RFP is faster and pulls in even fewer people.

Interviewer: So if you had to name the thing people get wrong about RFPs, what is it?

RFPLead: They think it's a writing exercise, that winning is about crafting brilliant answers each time. It isn't. It comes down to two things. First, triage. Saying no to the wrong ones, because a firm that bids everything mobilizes constantly and does everything badly. And second, the library, answering most of it from vetted content so you're not convening the whole firm for every questionnaire. The failure mode that genuinely hurts a firm is treating every RFP as a fire drill that yanks your investment team off their day job. Done right, an RFP is mostly assembly plus a little expert input on the margins. Done wrong, it's a tax on the entire firm. And keeping that library current and the performance data clean is mostly manual today, so that's exactly where I'd want better tooling.

Interviewer: That's a great place to end it. Really helpful, thank you.

RFPLead: My pleasure. It's a part of the business people don't see, so it's nice to explain how it actually holds together.

Keep exploring

A plans examiner maps multi-department review, resubmit loops, inspections, and final sign-off.

Watch

A treasury lead maps cash forecasting across funds and entities, and where it breaks down.

Watch

A brokerage account manager walks through COI issuance while the process maps itself; including the automation nobody had scoped.

WatchSapeum is designed with enterprise-grade security practices from the ground up: encryption at rest and in transit, role-based access controls, and auditable change history.

Everything you just saw runs on real workshops, not staged demos. Bring a process of yours and see for yourself.

Request a demo