Process interview demo Video

Building permits: submission to certificate of occupancy

A plans examiner maps multi-department review, resubmit loops, inspections, and final sign-off.

WatchAn investor relations lead walks a new limited partner from indication of interest to a funded, reporting investor: vehicle selection and eligibility (accredited / qualified purchaser, ERISA), KYC/AML and tax forms, subscription docs and side letters, fund-administrator setup, and the capital call and ongoing reporting that follow, with the manual handoffs and data-quality gaps that bite later.

Interviewer: Thanks for doing this. I'd love to walk through how you onboard a new investor, start to finish, the way you'd explain it to someone new on the IR team. Wherever you want to start.

IR: Sure. So onboarding a new LP, a limited partner, touches a lot of the firm. My team in IR, compliance, legal, and our fund administrator. People think of it as paperwork, and there's plenty of that, but really it's the start of a relationship that's going to run for ten years or more, so getting it right at the beginning matters enormously. Let me start where it starts, which is the indication of interest.

Interviewer: That's during the fundraise?

IR: Right. During the raise, a prospective investor signals they want in, and I log it in our CRM. Who they are, how much they're looking to commit, and which vehicle they belong in. And that last part matters right away, because a US pension is going into a different structure than an offshore investor or a high-net-worth individual. Onshore fund, offshore feeder, the structure decides which document set they get. So the very first call is really "what kind of investor is this, and where do they fit."

Interviewer: And then you check they're allowed to invest?

IR: Eligibility, yeah. We have to confirm they qualify. Accredited investor, qualified purchaser, qualified client, depending on the fund. We check their jurisdiction, and whether it's benefit-plan money, because ERISA brings its own rules. There's a threshold where, if too much of the fund is ERISA money, it changes how the whole fund is treated. So we're screening for all of that before we get too far.

Interviewer: Okay, they qualify. Then the documents.

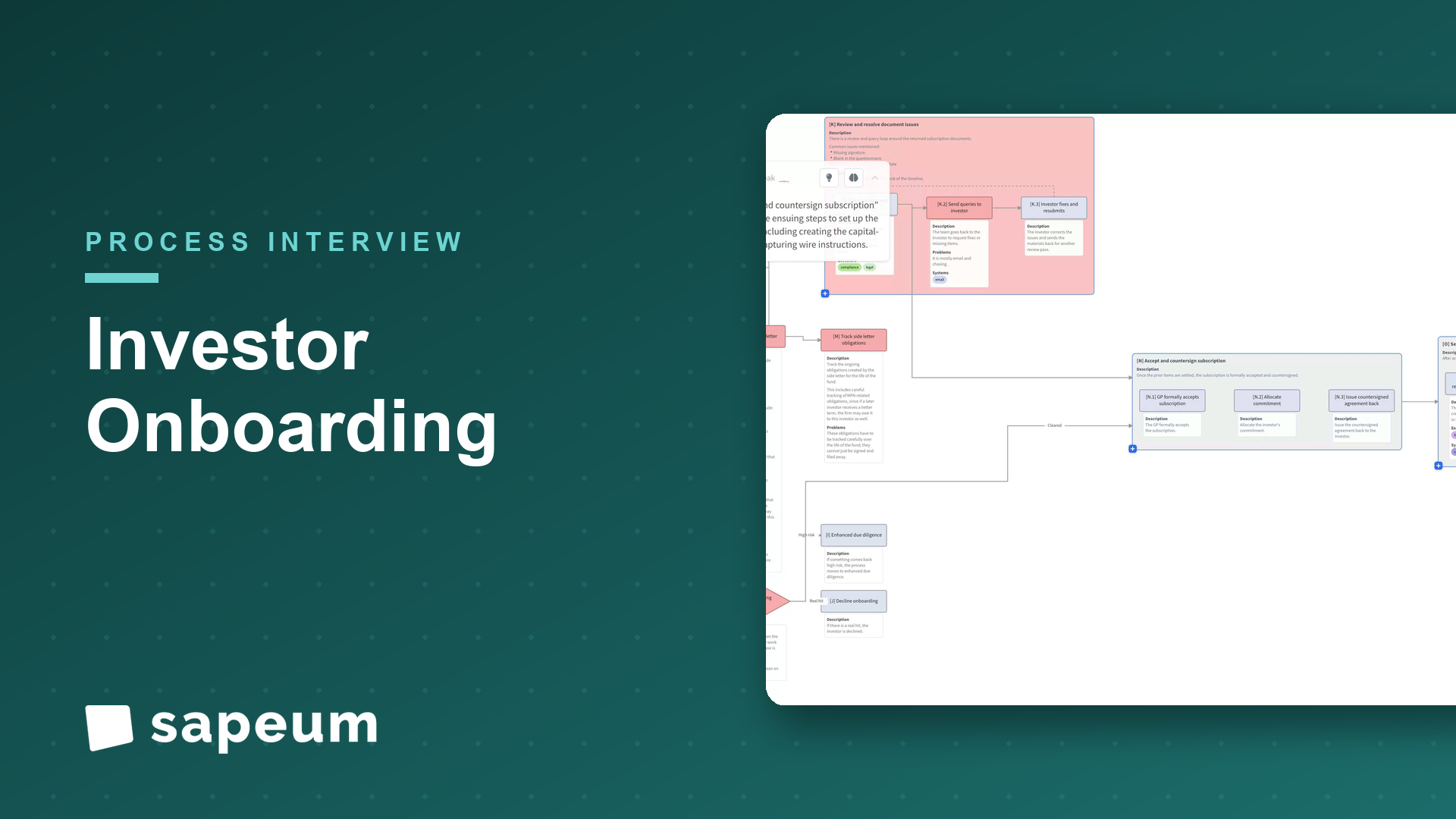

IR: Then we issue the subscription package, the subscription agreement and an investor questionnaire, and these days that's usually through a sub-doc platform rather than paper. In parallel, compliance kicks off KYC and AML. That's collecting beneficial ownership, who actually owns this entity, source of funds, and screening everyone against sanctions and PEP lists. If something comes back high-risk, we go to enhanced due diligence. If it's a real hit, we decline. We also collect tax forms at this stage, the W-9 or the W-8 series, FATCA classification, CRS self-certification.

Interviewer: That's a lot of collecting. Does it usually come back clean?

IR: Almost never on the first pass, honestly. There's always a missing signature, a blank in the questionnaire, an entity document that's out of date. So there's a review-and-query loop. Compliance and legal go through it, we go back to the investor, they fix it, it comes back. That back-and-forth eats a real chunk of the timeline, and it's mostly email and chasing. It's the least glamorous part, and probably where we lose the most days.

Interviewer: And then there's the negotiation you mentioned?

IR: For the bigger investors, yes, side letters. A large institutional LP will negotiate one: maybe a fee break, specific reporting they want, co-investment rights, transfer rights, most-favored-nation clauses. Legal handles the negotiation, but here's what people underestimate. Every side letter is a promise we have to keep for the life of the fund. An MFN clause means if we give a later investor a better term, we may owe it to this one too. So those obligations have to be tracked carefully, for years, not just signed and filed away.

Interviewer: Once all that's settled?

IR: We accept and countersign. The GP formally accepts the subscription, allocates their commitment, and issues the countersigned agreement back. Then we set them up in our systems. The fund administrator creates the investor record and their capital account, and we capture their wire instructions. And I'll flag one thing there. We always do a callback verification on banking details. Wire fraud in this industry is real. Someone spoofs an email with new wire instructions, so we call a known number to confirm. We never just take it off an email.

Interviewer: Good. So now they're in the system.

IR: Now they're in, and we bring them into the capital call schedule and issue their first drawdown. We don't take the whole commitment at once, we call capital as we need it. We reconcile the money when it lands. And if they're joining at a later close, there's an equalization. They have to compensate the earlier investors who've already been funding the fund, usually with an interest payment. That math runs through the administrator.

Interviewer: And then you actually set them up as an ongoing investor.

IR: Right, which is really the point. We provision their access to the investor portal: statements, capital account, documents, and we set who their reporting contacts are and what they're allowed to see. IR introduces the relationship manager, and we agree on how they like to communicate and how often. Then we stand up their reporting. The quarterly capital-account statements, capital-activity notices, fund financials, and their tax reporting, the K-1 schedule. So from here on, they're getting a steady cadence of reporting.

Interviewer: And it keeps going from there.

IR: It does. Ongoing client relations. Ad hoc requests, audit confirmations, the occasional transfer of their interest, periodic re-screening for AML. And then the periodic compliance and regulatory layer. KYC refreshes, regulatory reporting like Form PF or AIFMD that needs investor data, the annual audit, the annual tax package. That part never really ends. It just cycles every year.

Interviewer: So if you had to name the thing people get wrong about investor onboarding, what is it?

IR: They think it ends when the money arrives. Like, they funded, we're done, onboarding complete. But onboarding isn't the money. It's the data and the obligations you set up around it. The information we capture at the start, and how cleanly we capture it, drives every statement, every tax form, every regulatory filing for the next decade. And the side-letter promises we make have to be honored that whole time. So if the onboarding data is messy, or a side-letter obligation gets lost, it doesn't bite you that day. It bites you quietly, in every reporting cycle, for years. The skill is treating onboarding as laying the foundation, not clearing a paperwork hurdle. And honestly a lot of it still runs on email, spreadsheets, and chasing documents, so it's an area where better systems would save real time.

Interviewer: That's a great place to end it. Really helpful, thank you.

IR: Of course, happy to walk through it. There's a lot of hidden depth to it, so it's nice to lay it out.

Keep exploring

A plans examiner maps multi-department review, resubmit loops, inspections, and final sign-off.

Watch

A treasury lead maps cash forecasting across funds and entities, and where it breaks down.

Watch

A brokerage account manager walks through COI issuance while the process maps itself; including the automation nobody had scoped.

WatchSapeum is designed with enterprise-grade security practices from the ground up: encryption at rest and in transit, role-based access controls, and auditable change history.

Everything you just saw runs on real workshops, not staged demos. Bring a process of yours and see for yourself.

Request a demo