Process interview demo Video

Building permits: submission to certificate of occupancy

A plans examiner maps multi-department review, resubmit loops, inspections, and final sign-off.

WatchA fund controller at a private-capital firm walks through striking NAV end to end: cutoff, pricing liquid and illiquid positions, the valuation committee, accruals, leverage and FX, reconciliation, allocation and per-class NAV, sign-off and publish. It's struck monthly today, and the process strains against newer evergreen and semi-liquid products that need a daily NAV.

Interviewer: Thanks for sitting down. I want to walk through how you actually calculate NAV, end to end, the way you'd explain it to a new analyst on the team. Wherever you want to start.

Controller: Sure. So NAV, net asset value, is at its simplest just what the fund is worth, divided by the units. And I want to be honest up front, because it colors everything I'm about to describe. Today we strike NAV monthly, quarterly for some vehicles. But our newer products, the evergreen, semi-liquid stuff we're selling into the wealth channel, those really need a daily NAV. And our current process was never built to run every single day. So keep that in the back of your mind, because it's the tension sitting underneath the whole thing. Let me start at the cutoff.

Interviewer: The cutoff being the start of a NAV run?

Controller: Right. We set the valuation date and we lock the books for the period, so nothing else posts into that window. Then we capture all the activity since the last NAV. Trades, new fundings, loan paydowns, the capital activity, subscriptions and redemptions, and expenses. Getting a clean, complete picture of what happened is step one, and even that takes coordination across a few teams.

Interviewer: Then you price everything?

Controller: Then we price, and this splits into two very different worlds. The liquid positions, anything with an observable market price, we mark off the data feeds, straightforward. But a lot of what we hold is illiquid. Private loans, private equity. There's no screen price for those, so we value them per our valuation policy. Models, comparables, what accountants call level-three assets. Some of them we send to an independent pricing vendor for a third-party mark. That illiquid valuation is the genuinely hard, judgment-heavy part.

Interviewer: And someone signs off on those marks?

Controller: The valuation committee. Any material or illiquid mark gets reviewed and approved per policy. It's a governance step, deliberately so. If a mark looks stale, or someone disagrees, it goes back for re-review. And notice that's a committee, with meetings and a cadence. That works beautifully once a month. It is not something you can convene every morning before breakfast, which is part of why daily is so hard.

Interviewer: Okay, marks are set. What else goes into the number?

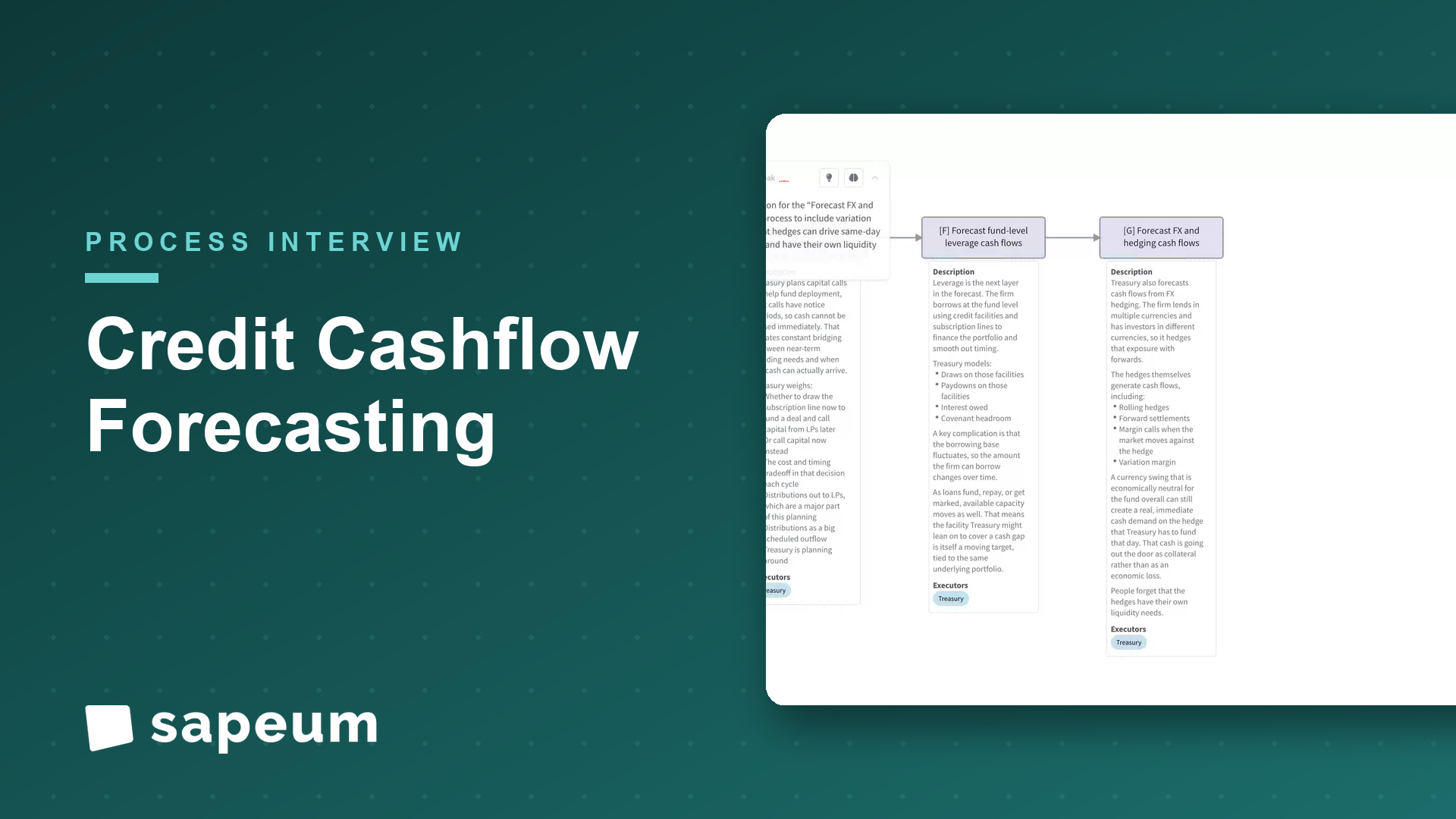

Controller: Then the accruals, which people outside finance always underestimate. We accrue income: interest, and in credit that includes things like PIK, payment-in-kind, OID, amortizing fees and discounts over the life of a loan. Then we accrue expenses and fees. The management fee, the incentive fee or carry, which has its own hurdle and crystallization logic, plus fund expenses, admin, audit, legal. Then leverage. We have to value the fund's debt and its subscription lines and the interest accruing on them. And then FX. We revalue everything that isn't in our base currency, and the hedges against it, at the period's rates.

Interviewer: That's a lot of moving pieces before you even get a total.

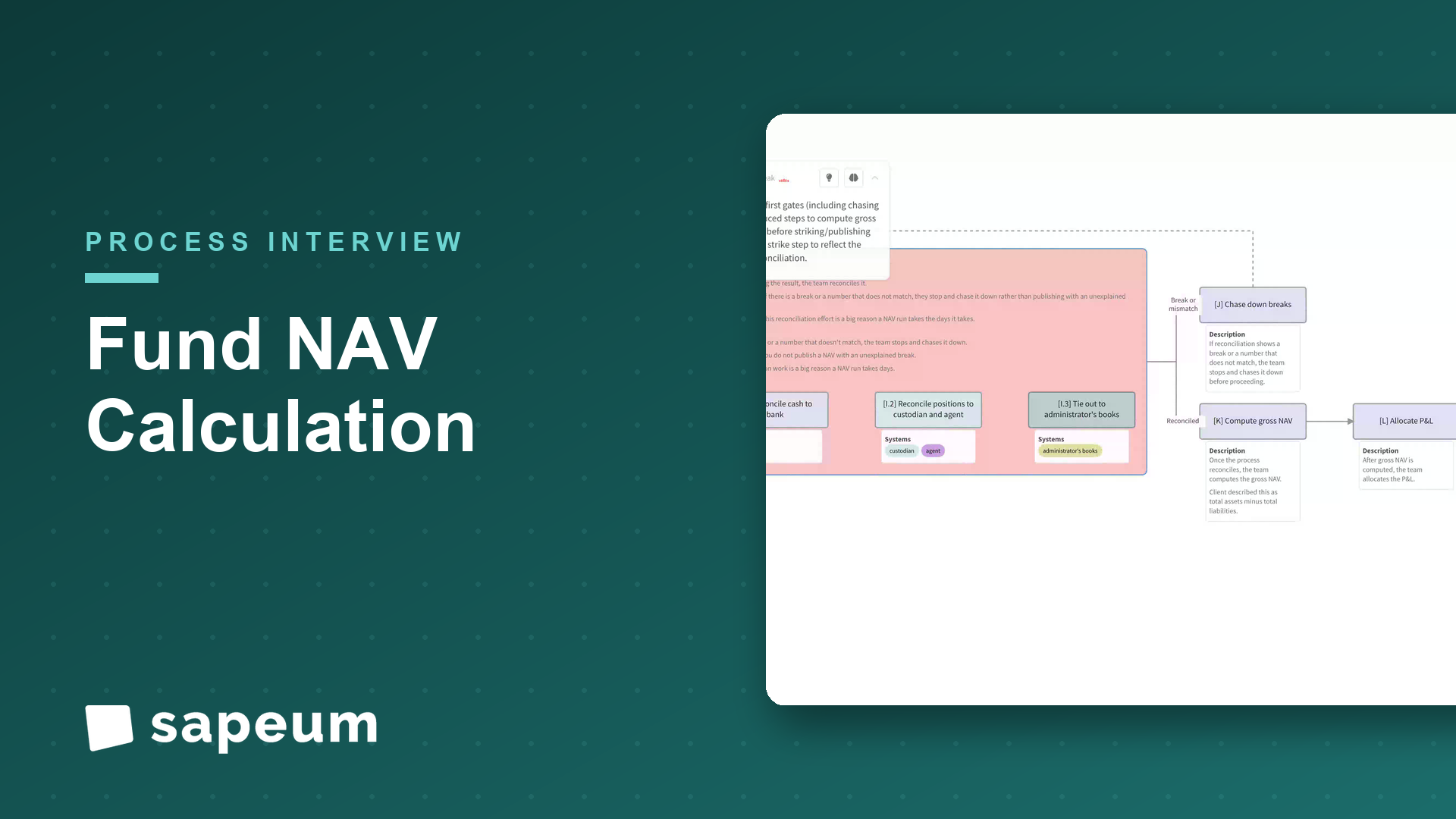

Controller: It is, and before we trust any of it, we reconcile. Cash to the bank, positions to the custodian and the agent, and everything ties out to the administrator's books. If there's a break, a number that doesn't match, we stop and chase it down. You do not publish a NAV with an unexplained break. That reconciliation is a big reason a NAV run takes the days it takes.

Interviewer: And once it reconciles?

Controller: Then we compute the gross NAV, total assets minus total liabilities, and then we allocate the P&L. That's not one number for everyone. We split it across share classes, series, sometimes investor by investor, because of series accounting, equalization, and different fee terms. Then we divide down to a NAV per unit for each class. And for the semi-liquid funds, that per-unit number isn't just reporting. It's the actual price people buy and sell at. So it has to be right.

Interviewer: Then it goes out.

Controller: Then review and sign-off under dual control. The controller and the administrator both review, nobody strikes a NAV on their own. We generate the investor capital statements, and we publish. We strike the subscription and redemption prices and feed all the downstream reporting. And then a month later we do the whole thing over again.

Interviewer: So come back to the daily piece. Why can't this just run daily?

Controller: Because every hard step I described assumes time. The illiquid marks lean on a committee that meets monthly. The reconciliation involves people chasing breaks. The accruals and the FX and the allocations are stitched together across systems and spreadsheets with manual checkpoints. Running that once a month, we can be careful. Compressing the whole chain, the valuation, the governance, the reconciliation, the allocation, into a single day, every day, with the same accuracy? That's the unsolved problem. The market's moving toward daily because that's what the wealth channel and the evergreen products demand, and we know we need to get there. We're just not there yet, and you can't get there by asking people to do the monthly process thirty times faster.

Interviewer: So if you had to name the thing people get wrong about NAV, what is it?

Controller: They think it's arithmetic. Assets minus liabilities, divide by units, done. But the arithmetic is the easy five percent. The real work is the illiquid valuations, the fee and carry accruals, the FX and the hedges, and the reconciliation that has to be clean before you'll stand behind the number. Because for a lot of our funds that number is the price investors transact at, so being wrong isn't an inconvenience, it's a real problem. And the thing making it genuinely hard right now is frequency. We've built a careful monthly process, and the business is asking for daily. That gap, between the rigor the number requires and the speed the products now demand, that's the whole challenge, and it's exactly where better tooling would change the game.

Interviewer: That's a great place to end it. Really helpful, thank you.

Controller: My pleasure. It's a deceptively deep process, so it's good to talk through it properly.

Keep exploring

A plans examiner maps multi-department review, resubmit loops, inspections, and final sign-off.

Watch

A treasury lead maps cash forecasting across funds and entities, and where it breaks down.

Watch

A brokerage account manager walks through COI issuance while the process maps itself; including the automation nobody had scoped.

WatchSapeum is designed with enterprise-grade security practices from the ground up: encryption at rest and in transit, role-based access controls, and auditable change history.

Everything you just saw runs on real workshops, not staged demos. Bring a process of yours and see for yourself.

Request a demo