Process interview demo Video

Building permits: submission to certificate of occupancy

A plans examiner maps multi-department review, resubmit loops, inspections, and final sign-off.

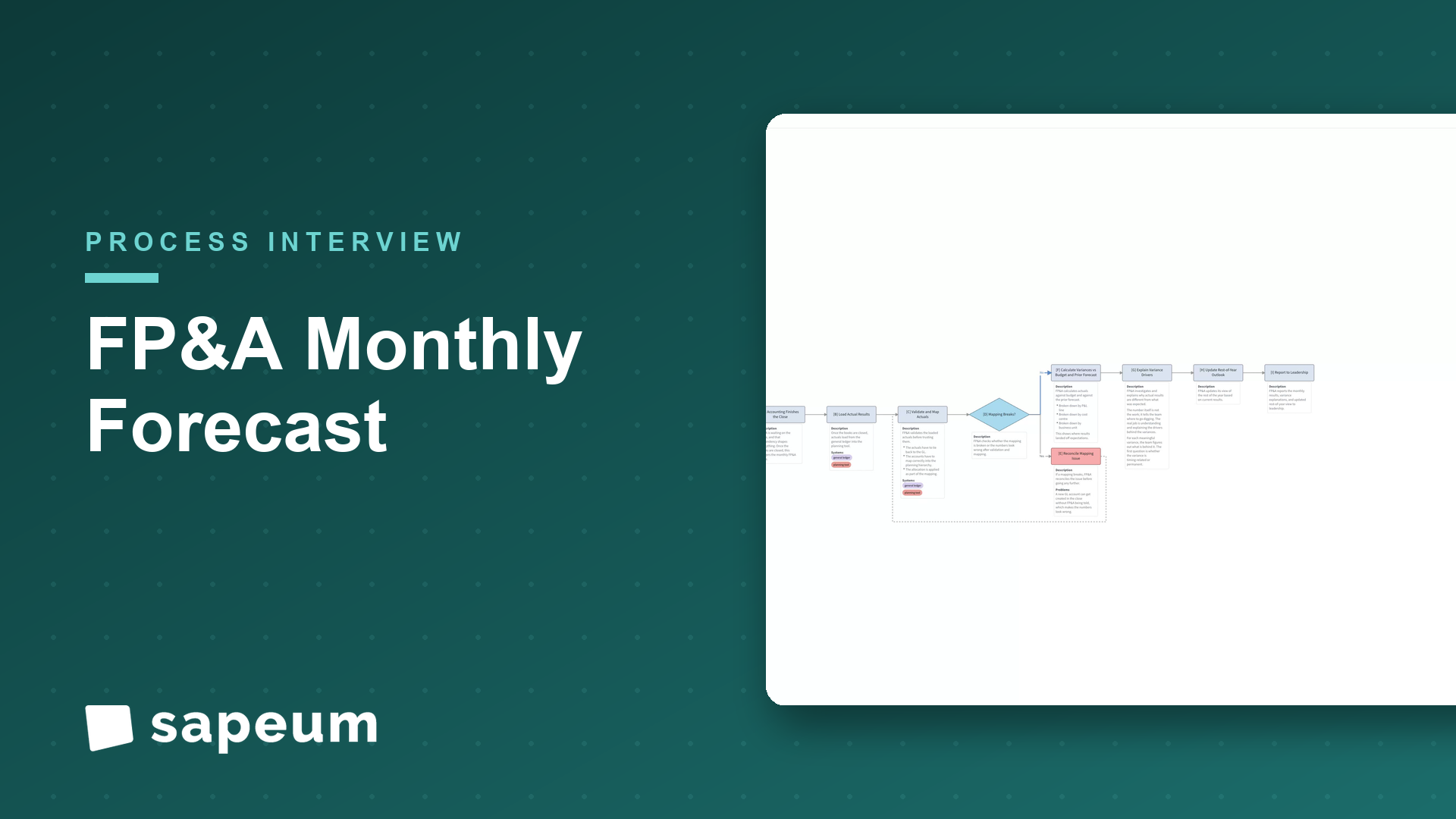

WatchAn FP&A lead at a B2B enterprise walks through the recurring monthly cycle: actuals load after close, validate and map, variance calculation and investigation, business-partner reviews, reforecast (revenue, headcount, opex), consolidate, reconcile to plan, the reporting package, sign-off, the monthly business review, and action tracking: candid that data wrangling eats the time.

Interviewer: Thanks for doing this. I'd love to walk through your monthly FP&A cycle, start to finish, the way you'd explain it to a new analyst joining the team. Wherever you want to start.

FPA: Sure. So the monthly cycle is really the heartbeat of FP&A. Every month we load what actually happened, explain why it's different from what we expected, update our view of the rest of the year, and report all of that to leadership. It's separate from the annual budget and from the longer-range strategic stuff. This is the recurring rhythm. And it starts the moment accounting finishes the close.

Interviewer: So you're waiting on the close.

FPA: We are, and that dependency shapes everything. Once the books are closed, the actuals load from the general ledger into our planning tool. And I'll be honest, when the close runs late, our whole timeline compresses, because leadership still wants the reporting on the same date regardless. So a slow close means a frantic FP&A week. That's just the reality of going second.

Interviewer: Okay, the actuals are in. What's the first thing you do with them?

FPA: We validate and map them before we trust them. The actuals have to tie back to the GL, and the accounts have to map correctly into our planning hierarchy, with the allocations applied. If a mapping breaks, say a new GL account got created in the close and nobody told us, the numbers look wrong and we have to reconcile it before we go any further. It's unglamorous, but if you skip it you end up analyzing garbage.

Interviewer: Then you compare to the plan?

FPA: Then the variances, yes. We calculate actuals against budget and against our prior forecast, broken down by P&L line, by cost center, by business unit. That tells us where we landed off expectations. But the number itself isn't the work. The number just tells you where to go digging. The real job is the next step, investigating why.

Interviewer: Tell me about that.

FPA: So for each meaningful variance, we figure out what's behind it. And the first question is always, is this timing or is it permanent. If marketing underspent because an event slipped from March to April, that's timing, it'll catch up. If we lost a big customer, that's permanent and it changes the forecast. Those are completely different stories, and confusing the two is how you misread the business. To get the truth, we don't guess from our desks, we go to the business partners.

Interviewer: The department leaders.

FPA: Right. We sit down with the department heads and the BU leaders, and we get the actual drivers and their commentary. They know why their number moved in a way the ledger never will. And honestly that business partnering is the most valuable part of the job and the part you can't automate. A good FP&A person is in those conversations constantly, not just running reports. Then we take everything we've learned and reforecast.

Interviewer: What does the reforecast actually involve?

FPA: We update our rolling view of the year based on the actuals plus the latest expectations. Some of it is bottoms-up, the owners submit their updated numbers, and some of it is top-down adjustments we make centrally. The biggest pieces are revenue, headcount, and the rest of opex. Revenue we model with sales and RevOps, new bookings, renewals, churn, how fast new reps ramp. That's the hardest line to predict and the most important.

Interviewer: And headcount, you mentioned.

FPA: Headcount is the one I watch hardest, because for a B2B enterprise people are by far the largest cost. So we forecast the hiring plan, expected attrition, and crucially the timing, because a role you planned to fill in January that doesn't get filled until June is a big swing in the numbers. We work that with HR and recruiting. Then the rest of opex, vendors, marketing programs, travel, plus the capital and depreciation side.

Interviewer: Then it all comes together.

FPA: Then we consolidate. We roll the cost centers, the business units, and the legal entities up into one company forecast, with the intercompany eliminations and the currency translation if we're multi-entity. And once we've got the consolidated reforecast, we reconcile it back to the plan and to any external guidance we've given, and we flag the gaps. If we're forecasting below plan, the conversation immediately becomes what are we going to do about it, what actions close the gap. That's the part leadership actually cares about.

Interviewer: And you package it up.

FPA: We build the monthly reporting deck. The P&L, the variance bridges that explain the walk from plan to actual to forecast, the KPIs, forecast versus plan, and the written commentary that tells the story. The FP&A lead and the CFO review it, and we sharpen the narrative, sometimes the numbers get questioned and we go back and rework. Then we present it in the monthly business review with leadership, and feed the board reporting when that's due.

Interviewer: Is that the end of the cycle?

FPA: Almost. The last piece that's easy to drop is action tracking. The business review generates decisions and follow-ups, and we capture those and carry them forward, because next month we'll want to know whether the actions we agreed actually moved anything. And then we maintain the model and do the whole thing again. It genuinely never stops, you finish one cycle and the next close is right behind it.

Interviewer: So if you had to name the thing people get wrong about FP&A forecasting, what is it?

FPA: They think it's about the model, that forecasting is a spreadsheet skill. The model matters, but two things matter more. First, the explanation, understanding why the numbers moved and whether it's timing or real, because a forecast nobody can explain is useless to a decision-maker. And second, the business partnering, because the forecast is only ever as good as the inputs you get from the people running the business, and getting honest, timely drivers out of them is the actual craft. And I'll add the painful truth, which is that we spend far too much of the month just assembling and reconciling data, loading actuals, fixing mappings, stitching spreadsheets together, when that time should be going into the analysis. So the opportunity isn't a fancier model. It's getting the data plumbing out of the way so the team can spend the month thinking instead of wrangling.

Interviewer: That's a great place to end it. Really helpful, thank you.

FPA: My pleasure. It's a cycle that's relentless but kind of satisfying, so it's nice to lay out how it really works.

Keep exploring

A plans examiner maps multi-department review, resubmit loops, inspections, and final sign-off.

Watch

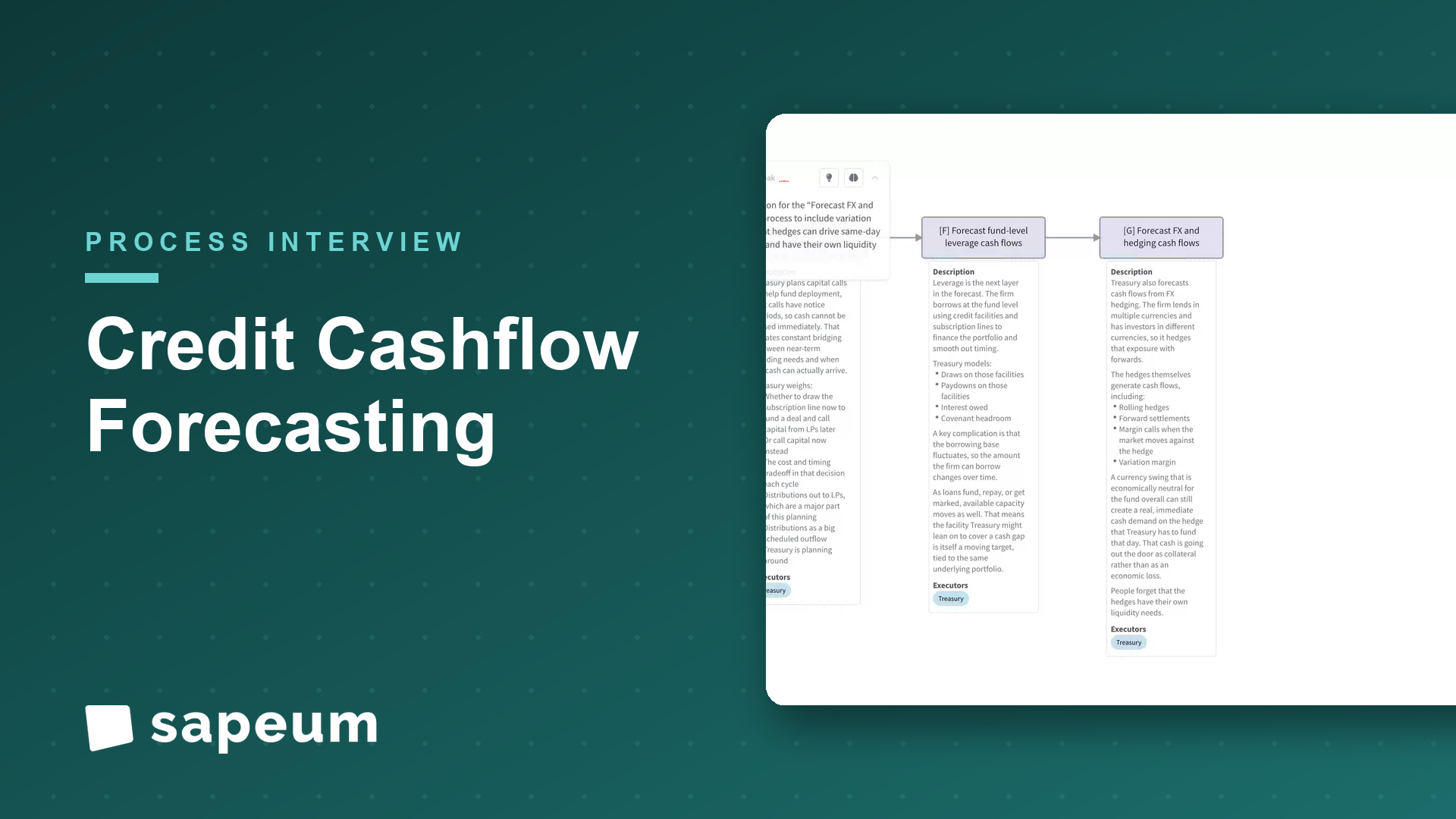

A treasury lead maps cash forecasting across funds and entities, and where it breaks down.

Watch

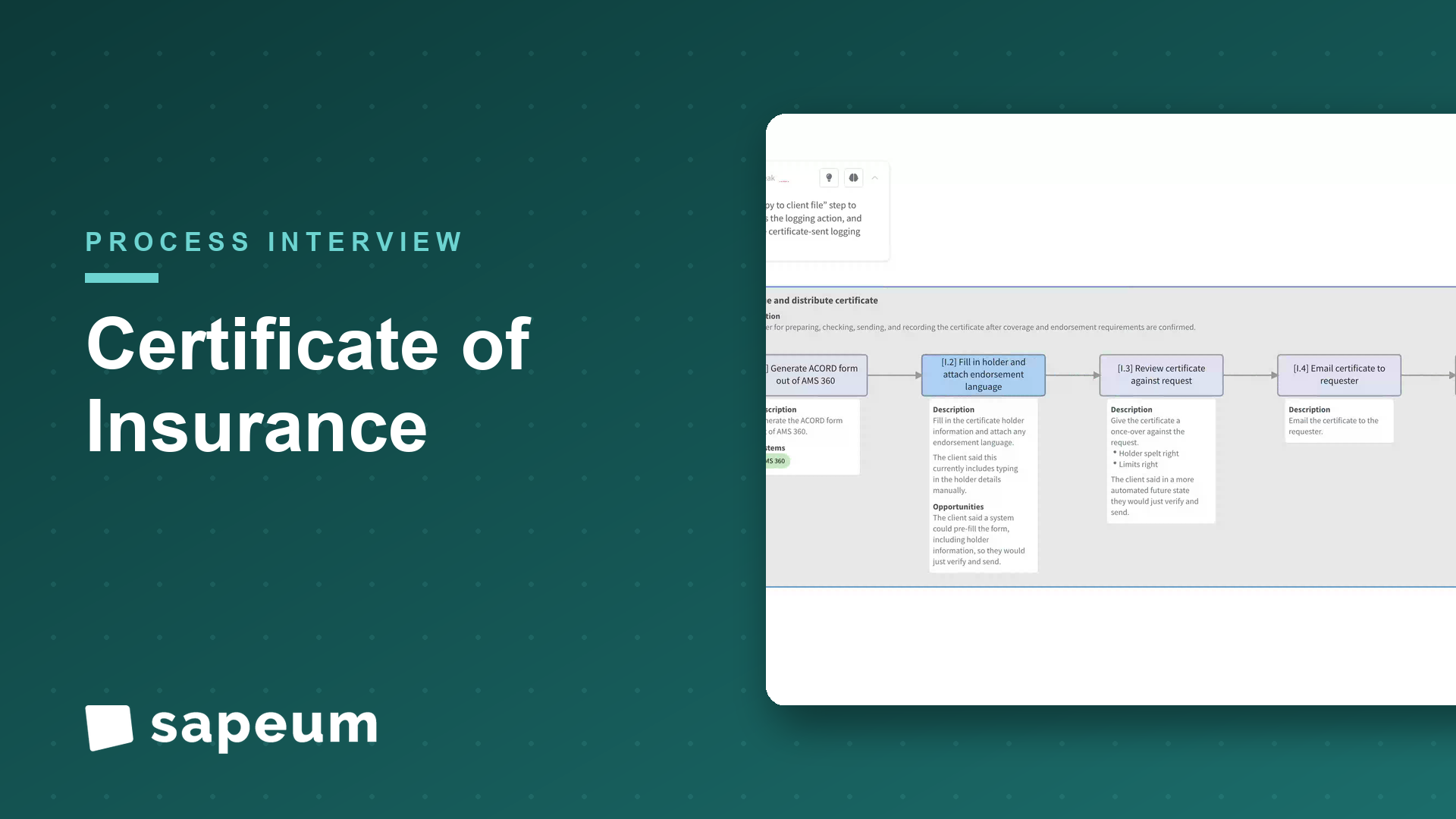

A brokerage account manager walks through COI issuance while the process maps itself; including the automation nobody had scoped.

WatchSapeum is designed with enterprise-grade security practices from the ground up: encryption at rest and in transit, role-based access controls, and auditable change history.

Everything you just saw runs on real workshops, not staged demos. Bring a process of yours and see for yourself.

Request a demo